| Name: |

MATP6640/ISYE6770

Linear Programming

Spring 2014

Midterm Exam, Friday, April 11, 2014.

Please do all four problems. Show all work. No books or calculators allowed. You may use any result from class, the homeworks, or the texts, except where stated. You may use one sheet of handwritten notes. The exam lasts 110 minutes.

| Q1 | /25 | |

| Q2 | /25 | |

| Q3 | /25 | |

| Q4 | /25 | |

| Total | /100 |

Throughout, the standard primal-dual LP pair is

where A is m × n and the vectors are dimensioned appropriately. The rank of the matrix A is m. The dual slack variables are defined as s := c - AT y.

where b1 and b2 are parameters.

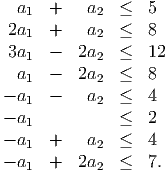

![[ ]

a1

a

2](midterm142x.png) for the matrix A, all with cost

c = 11. The corresponding x variables are nonnegative. These additional columns all

satisfy the constraints

for the matrix A, all with cost

c = 11. The corresponding x variables are nonnegative. These additional columns all

satisfy the constraints

Is the basic feasible solution from part (1a) optimal in the full problem?

(this page intentionally left blank)

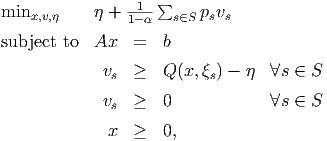

| (1) |

where α is a parameter, Q(x,ξs) is the recourse cost for the first stage decision x in scenario s, η is a scalar variable, and v ∈ IRr.

Assume 0 < 1 - α < ps for all s ∈ S.

(this page intentionally left blank)

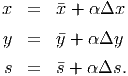

. Let the

direction (Δx, Δy, Δz) satisfy the system of equations

. Let the

direction (Δx, Δy, Δz) satisfy the system of equations

where and are diagonal matrices with ii = i and ii = i for i = 1,…,n. Let α be a step length and update

Show that xT s = n.

(Hint: You will need to exploit the fact that rank(A) = m in this question. Equivalently, the rows of A are linearly independent.)

(this page intentionally left blank)